Build equity, tax benefits, and stable housing.

Get your home without sacrificing your financial stability.

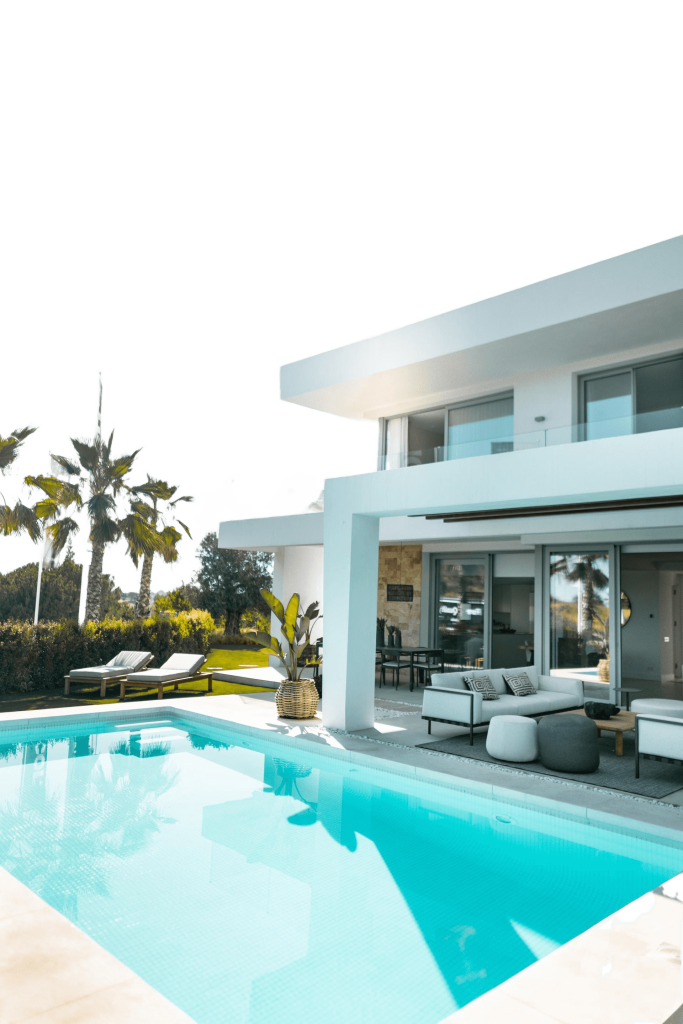

We’ve helped hundreds of people buy their dream home with our mortgage options. You can choose from different rates, loan types, and down payment plans. Homeownership lets you build equity, save on taxes, and have stable housing costs. You can get your home without hurting your finances. Contact us today and we’ll find the best mortgage for you

It’s your mortgage. Use it.

Take Cash Out

Making all those monthly payments is now plus for you. You now have equity in your home. You can use that equity when you need it, family emergency, renovations, or payoff debts. It’s yours, use it .

Lower Payment

Why not continue to own and pay less. Payless out is more in your pocket. Use the funds to help you with other things like college saving, or retirement investments. It’s your money use it how you need too.

Flexible Terms

Get the terms that befit your plan. Want to end the payments earlier, adjust the terms and pay it off faster. This will save you thousands of dollars in interest. Our lenders offer and we can secure custom offers.

Numbers Speak

Happy Customers

24 Hours

Access your loan online and on the go.

More than 90%

Successful Applications

FAQ

A Few Common Mortgage Questions.

➤ How much home can I afford?

Many people start by determining what they can afford as a monthly payment. A common starting point is to calculate 25% of your gross monthly income to help determine a manageable monthly mortgage payment.

➤ What parts of my finances does a mortgage lender review?

A lender will check your credit score and history, your debt-to-income ratio, which is a measurement of the amount of debt you have compared to your income, and take a general look at how much money you have in checking and savings accounts in order to be confident you’ll be able to pay for your mortgage, taxes, and other costs associated with buying a home.

➤ What is the minimum down payment for conventional, FHA, and VA loans?

Most lenders offer several low-down payment options, including conventional loans (those not backed by a government agency).

Conventional fixed-rate loans are available with a down payment as low as 3%.

- Keep in mind that with a low down payment mortgage insurance will be required, which increases the cost of the loan and will increase your monthly payment. We’ll explain the options available, so you can choose what works for you.

- Talk with a home mortgage consultant about loan amount, loan type, property type, income, first-time homebuyer, and homebuyer education requirements to ensure eligibility.

FHA loans are available with as little as 3.5% down.

- FHA loans have the benefit of a low down payment, but you’ll want to consider all costs involved, including up-front and long-term mortgage insurance and all fees.

- Be certain to ask your home mortgage consultant to help you compare the overall costs of all your home financing options.

VA loans offer low- and no-down-payment options for eligible veterans and other eligible borrowers.

➤ What other costs are part of my mortgage?

Your monthly mortgage payment typically will include principal and interest on the mortgage, as well as homeowners’ insurance and property taxes if your mortgage payment includes escrow. Depending on your down payment and loan type, you may also have to pay private mortgage insurance as part of your monthly mortgage payment.

➤ After preapproval, how long does it take to close?

The number of days from application to approval will vary for purchase and refinance home loans. The timeline is generally 30-90 days.

➤ What is an origination charge?

The origination charge is the amount charged for services performed on the initial loan application and loan processing. This includes all charges (other than discount points) that lenders and brokers involved in the transaction will receive for originating the loan. It includes any fees for application, processing, underwriting services, and payments from the lender for origination.

➤ How much money will be required at closing?

The amount you’ll need to close your loan includes your down payment, closing costs, and prepaid escrow amounts for property taxes and insurance. Prior to closing, you’ll be informed of the final amount.

Start Your Mortgage Application

Looking for a mortgage that fits your needs and budget? Contact us today and let our experts help you find the best option and get you approved fast.